May 2024 Commodities

Lumber posts modest gains, Steel mill products getting hammered, and construction costs still rising

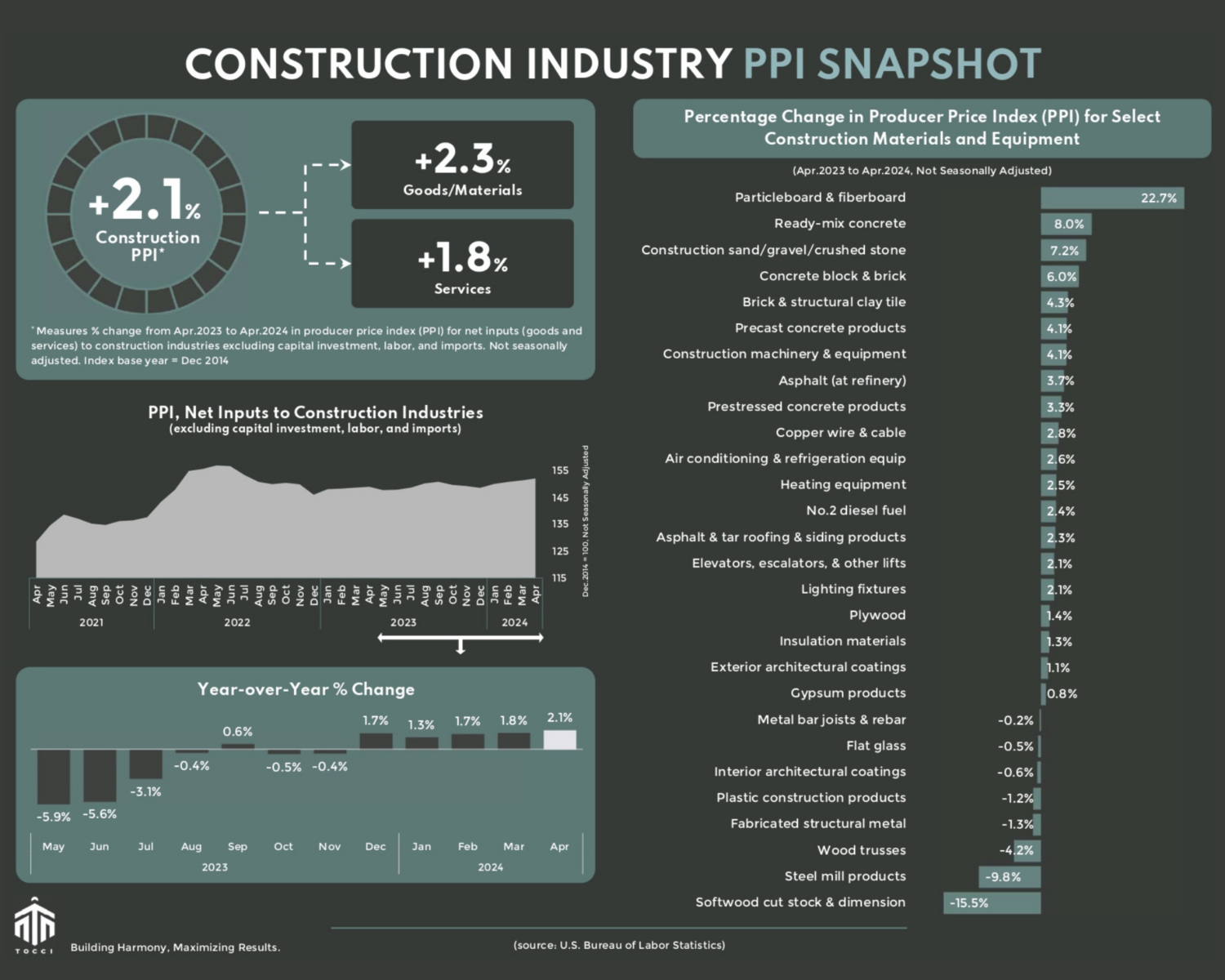

Construction costs continue to rise. In April, the Producer Price Index (PPI) for construction inputs – a broad measure of inflation in materials and services for construction – climbed by 0.5% from the previous month, scoring a 2.1% increase from a year ago.

LUMBER: Lumber futures have made posted gains over the past month, rising 7.9% and hovering around $540 per thousand board feet. The PPI for softwood lumber rose by 1.4% in April (month-over-month) but is up 7.5% over the past four months. Typically, lumber prices peak around this time due to heightened seasonal demand. However, a sluggish housing market has kept lumber prices subdued. The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI), which measures sentiment around home sales, fell to 45 in May, a six-point drop from April. This decline marks the first dip in builder confidence since November 2023.

New residential construction data from the U.S. Census Bureau shows that builders broke more ground in April with construction starts rising by 5.7% above March’s revised estimates. This surge was fueled by a dramatic 31.4% month-over-month increase in multifamily starts. Yet, when viewed across all segments, starts have stayed relatively flat year-over-year. Permits, a barometer of future construction activity, ticked up 3.5% year-to-date compared to the same period last year (not seasonally adjusted). However, the pace of year-over-year growth in permits has decelerated by 2%.

STEEL and others: Steel futures have faced significant pressure since the beginning of the year. U.S. flat-rolled steel prices have remained bearish for several months, with hot-rolled coil (HRC) futures still 33% below their peak at the end of 2023. By May, HRC futures had plunged below $800 per short ton. Entering a new down cycle, steelmakers responded in March with price hikes, aiming to lift minimum prices. Despite these efforts, prices have not stabilized, casting doubt on their ability to reverse the downward trend. If mills are unable to halt the decline, production cuts may be in the works. The PPI for steel mill products dropped by 2.7% in April from the previous month and plunged 9.8% year-over-year.

Electrification costs are on the rise, driven by a surge in copper prices. This escalation is due to a mix of supply shortages, investor speculation, the expansion of AI and demand for green energy. Copper futures are hitting all-time highs, propelled by increased demand from data centers and a burgeoning EV market. April’s PPI for copper wire and cable shot up by 5.2% from the previous month and 7.5% year-to-date. Similarly, the PPI for copper and brass mill shapes rose by 4.7% month-over-month and 6.7% year-to-date. With copper prices this high, don’t be surprised if security is heightened at construction sites – no one wants to see their wiring get nicked.

From laying the foundation of accurate construction cost estimations to erecting a fortress of value engineering, we’re here to scaffold your project. Let’s connect and cement some ideas together.

See below for a commodities snapshot, or click here for the full report.